As the United States moved from the turbulence of 2025 toward the uncertainty of 2026, one message emerged consistently from credible economic institutions: the economy was not entering a crisis, but neither was it returning to effortless stability. Growth remained possible, yet confidence depended on conditions that lay beyond headline numbers.

This transition period is best understood not through predictions, but through how authoritative institutions framed risks, assumptions, and constraints at the close of 2025. What follows is a disciplined synthesis of those perspectives grounded in official statements, baseline forecasts, and published assessments bridging what happened in 2025 with what professionals believe will matter most in 2026.

The Federal Reserve: Risk Management, Not Victory

The Federal Reserve entered 2026 emphasizing risk management over directional certainty. The December 2025 decision to reduce the federal funds rate by 25 basis points was accompanied by language that avoided triumphal framing. Instead, policymakers reiterated their dual mandate and stressed that both inflation and employment risks required continued monitoring (Federal Reserve, 2025).

In its statement, the Federal Open Market Committee reaffirmed that policy decisions would remain data-dependent, particularly with respect to labor market conditions and inflation persistence. This posture reflects an institutional acknowledgment that the economic environment had become more balanced in terms of upside and downside risks.

Notably, the Fed did not signal a rapid easing cycle. Rather, it underscored caution, noting that while inflation had moderated, it had not fully returned to target. At the same time, labor market indicators such as rising unemployment and declining job openings suggested that overtightening could carry costs.

What the Fed’s stance implies for 2026:

Economic stability depends less on stimulus and more on policy calibration. The central bank’s priority is to avoid sharp missteps, reinforcing predictability rather than acceleration.

The International Monetary Fund: Moderate Growth with Structural Caveats

The International Monetary Fund has consistently framed the U.S. outlook within a context of relative resilience among advanced economies, while cautioning against uneven outcomes. In its World Economic Outlook released in late 2025, the IMF projected U.S. growth to remain around 2 percent in the near term, supported by productivity gains and sustained consumption (IMF, 2025).

However, IMF analysis emphasizes that growth quality matters as much as growth rate. The institution highlighted that productivity-enhancing investments particularly in digital infrastructure and artificial intelligence are contributing to output expansion, but that these gains are capital-intensive and may not translate evenly into employment or income growth.

The IMF also stressed that policy uncertainty especially around trade and fiscal governance remains a material downside risk. While not forecasting a downturn, the Fund cautioned that confidence-sensitive investment could be affected if uncertainty persists.

What the IMF’s outlook implies for 2026:

The U.S. economy is expected to grow, but distributional effects and confidence dynamics will shape how that growth is experienced by households.

The Congressional Budget Office: Baselines Assume Stability

From a fiscal and structural perspective, the Congressional Budget Office offers a more conditional view. CBO projections for 2026 are built on current-law assumptions, meaning they do not account for unforeseen policy disruptions such as government shutdowns or abrupt trade actions (CBO, 2025).

Under these assumptions, the CBO projects moderate economic growth and a gradual normalization of labor market conditions. However, the agency repeatedly emphasizes that its baseline outlook assumes institutional continuity regular appropriations, predictable fiscal operations, and no major external shocks.

Importantly, the CBO flags long-term challenges related to fiscal sustainability and demographic pressures, though these are framed as structural issues rather than immediate cyclical threats.

What the CBO’s framework implies for 2026:

Economic outcomes are highly sensitive to governance quality. Stability is not automatic; it is an assumption that must be met.

Image

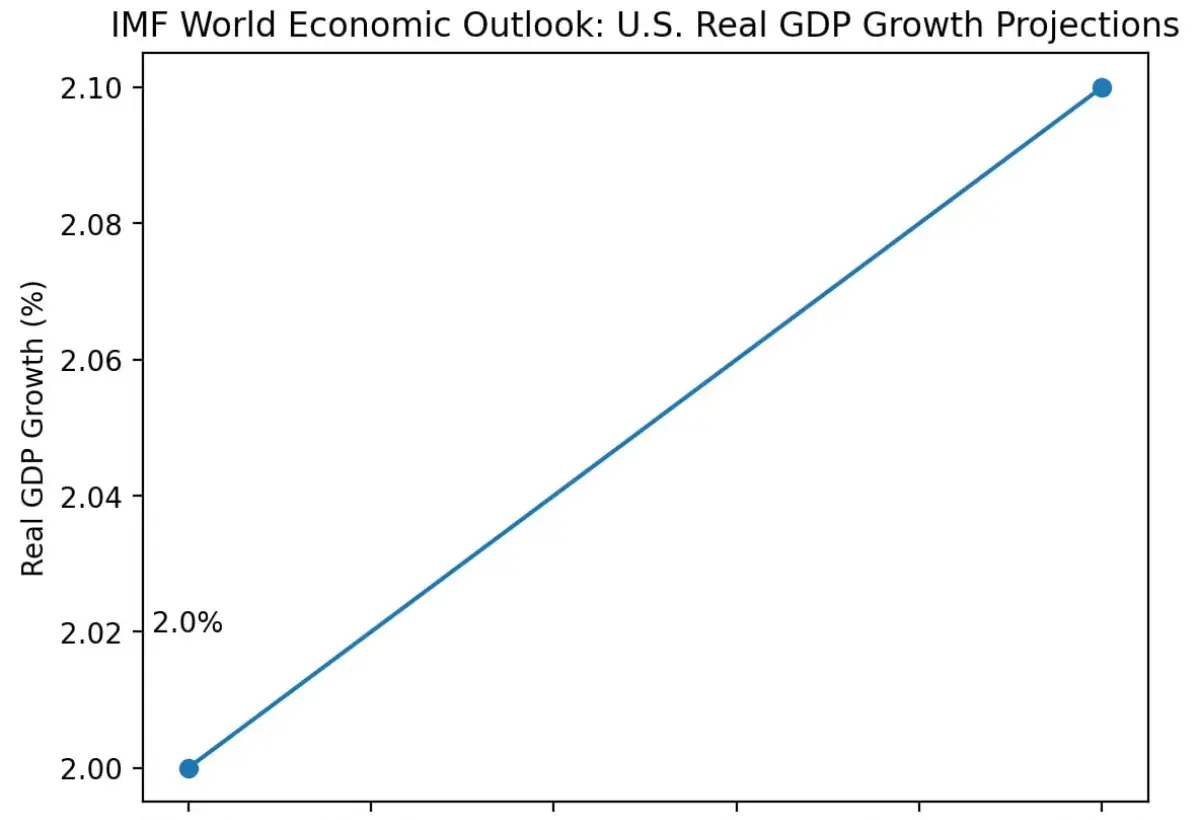

Figure 1. Author’s visualization based on International Monetary Fund World Economic Outlook projections shows U.S. real GDP growth of approximately 2.0 percent in 2025 and 2.1 percent in 2026, reflecting a modest upward revision in the IMF’s baseline outlook amid continued risks.

Source: International Monetary Fund, World Economic Outlook (October 2025).

According to the International Monetary Fund’s World Economic Outlook, U.S. real GDP growth is projected at approximately 2.0 percent in 2025 and 2.1 percent in 2026, representing a modest upward revision from earlier forecasts (International Monetary Fund, 2025). The IMF attributes this adjustment to resilient domestic demand and productivity-enhancing investment, while emphasizing that the outlook remains subject to downside risks, including policy uncertainty and global economic fragmentation. Rather than signaling a return to rapid expansion, the revised projections suggest a period of steady but cautious growth, reinforcing the IMF’s assessment that economic momentum can persist only if confidence and policy stability are maintained.

Labor market conditions at the end of 2025 provided important context for expert outlooks. Data from the Bureau of Labor Statistics showed that the unemployment rate had risen to 4.6 percent by November, while job growth slowed across several sectors (BLS, 2025). At the same time, data from Federal Reserve Bank of St. Louis (FRED) indicated that job openings had declined from earlier peaks, suggesting reduced labor demand even as layoffs remained limited.

Most professional economists interpret these signals as indicative of a cooling labor market, not a contraction. Wage growth has moderated, and hiring has become more selective, but there is no evidence of a broad labor collapse entering 2026.

What labor data imply for 2026:

Households may feel increased caution even if aggregate labor conditions remain historically healthy. Job security may matter more than job availability.

Market Economists: Confidence as a Constraint

Across market commentary grounded in official data, a recurring theme emerges: confidence has become a binding constraint. While financial conditions have stabilized and credit remains available, investment decisions are increasingly sensitive to policy clarity.

This perspective aligns with observed behavior in 2025, when businesses delayed expansion despite strong output data. The implication for 2026 is that capital allocation will favor environments with predictable rules and clear signals. Importantly, this is not framed as pessimism by professional analysts, but as prudence.

What market-oriented analysis implies for 2026:

Growth is feasible, but clarity amplifies momentum, while uncertainty suppresses it.

Image

Bridging Expert Analysis to Citizen Experience

For citizens who experienced 2025 as a year of contradiction, expert outlooks may seem detached. Yet their implications align closely with lived experience.

-

Moderate growth does not guarantee improved financial comfort

-

Cooling labor markets can feel restrictive even without job losses

-

Policy uncertainty directly affects household planning decisions

Executive Evidence Summary

The closing analysis of this article rests on consistent evidence from the United States’ principal economic authorities and international institutions. National output data from the Bureau of Economic Analysis confirmed that economic growth remained strong through much of 2025, with real GDP accelerating in the third quarter. At the same time, labor market indicators from the Bureau of Labor Statistics and Federal Reserve Economic Data showed clear signs of moderation, including a gradual rise in unemployment and a decline in job openings, pointing to cooling rather than contraction.

Policy developments contributed materially to the economic environment. Trade actions announced by the White House reintroduced uncertainty into global supply chains, while fiscal disruptions underscored the growing role of political risk in economic decision-making. In response, the Federal Reserve adjusted monetary policy in December, emphasizing a cautious, data-dependent approach as it balanced moderating inflation against softening labor conditions.

Looking forward, both the Congressional Budget Office and the International Monetary Fund project continued but moderate growth into 2026, contingent on policy stability and institutional continuity. These projections reinforce a central conclusion of this analysis: the U.S. economy retains the capacity to grow, but confidence depends on coherence between policy signals, economic performance, and household experience. Restoring that coherence will be essential for translating resilience into reassurance in the year ahead.

Author’s Reflection

The data reviewed suggest that the U.S. economy is transitioning from resilience toward recalibration as it moves into 2026. Institutional sources, including the Federal Reserve and the International Monetary Fund, point to continued but moderate growth, supported by productivity gains rather than renewed confidence. The IMF’s upward revision of U.S. growth reflects improved expectations, not acceleration. At the same time, labor market cooling and persistent policy uncertainty have weighed on household sentiment. The central challenge ahead is not economic capacity, but alignment restoring coherence between headline performance, policy signals, and lived experience. Confidence, more than growth alone, will shape the path forward.

Image

References

· Bureau of Economic Analysis. (2025). Gross domestic product, third quarter 2025: Initial estimate. https://www.bea.gov

· Bureau of Labor Statistics. (2025). The employment situation November 2025. https://www.bls.gov

· Congressional Budget Office. (2025). The budget and economic outlook: 2025 to 2035. https://www.cbo.gov

· Federal Reserve. (2025). Federal Open Market Committee statement, December 2025. https://www.federalreserve.gov

· Federal Reserve Economic Data. (2025). Labor market and macroeconomic indicators. https://fred.stlouisfed.org

· International Monetary Fund. (2025). World economic outlook. https://www.imf.org

White House. (2025). Fact sheet: Reciprocal tariff actions. https://www.whitehouse.gov

Thanks for these photos Bobby_sun, Pasja1000, and ojdClam on Pixabay.