Europe’s Economy in 2025: A Year of Durability and Decisions

2025 was not Europe’s comeback year but it was the year crisis ended, resilience held, and hard economic truths became impossible to ignore.

When economists reflect on Europe in 2025, they will not describe a year of dramatic growth or collapse, but rather one of adjustment, perseverance, and recalibration. For citizens, the experience was more ambivalent: moderate improvements in inflation and employment unfolded alongside persistent geopolitical tensions, cost-of-living pressures, and cautious public confidence. Against a backdrop of structural constraints and external risks, 2025 became a test of Europe’s economic resilience and social tolerance.

A Slow but Steady Recovery

At the core of Europe’s 2025 economic story was a modest but broad-based recovery.

According to the European Commission’s Autumn 2025 Economic Forecast, real GDP in the European Union was projected to grow by approximately 1.4 percent, with similar outcomes expected across the euro area once weaker external demand was accounted for. Growth was forecast to continue into 2026 and 2027 at comparable, though still subdued, rates. At the same time, employment continued to expand, keeping unemployment rates near historically low levels in many member states, as reported by Eurostat.

This pace of recovery reflected a gradual normalization following years of pandemic disruption and energy-driven shocks. While not rapid enough to feel transformative, it provided a sense of economic stabilization after prolonged uncertainty. For policymakers, the message was clear: Europe had regained its footing, but momentum remained fragile. Yet optimism was tempered by persistent structural challenges low productivity growth, demographic pressures, and external trade risks that limited the speed and breadth of the recovery.

Monetary Policy: Between Stability and Caution

For the European Central Bank, 2025 marked a transition from crisis management to measured stewardship. After an extended tightening cycle aimed at restoring price stability, the ECB maintained policy rates at restrictive but stable levels through much of the year, as inflation moved closer to the ECB’s 2 percent medium-term target.

ECB staff projections indicated that inflation was easing as energy and supply-side pressures diminished, though risks remained from services inflation and wage dynamics. Growth, meanwhile, was expected to remain positive but modest, underscoring the delicate balance between containing inflation and avoiding an unnecessary slowdown.

For economists, the ECB’s posture in 2025 signaled confidence that the worst inflationary pressures were behind Europe, while acknowledging that premature easing could undermine hard-won credibility. Monetary policy became less reactive and more anticipatory focused on managing risk rather than responding to crisis.

Trade, Tariffs, and External Headwinds

Europe’s recovery in 2025 unfolded amid a challenging global trade environment. According to assessments by the European Central Bank and the International Monetary Fund, elevated trade frictions particularly with major partners continued to weigh on export-oriented sectors such as manufacturing and capital goods.

While businesses gradually adapted to new tariff structures and supply chain realignments, uncertainty persisted. IMF forecasts were revised slightly upward during the year, reflecting resilience in domestic demand and front-loaded trade activity, but external demand remained a constraint on faster growth. These trade dynamics influenced corporate investment behavior, with firms taking a more cautious approach to expansion. The message from international institutions was consistent: Europe had absorbed the shock, but globalization had become less predictable and more politically contingent.

Geopolitics and Fiscal Choices: The Ukraine Equation

No factor shaped Europe’s economic and fiscal debates in 2025 more profoundly than the ongoing war in Ukraine.

The European Commission, in coordination with EU member states and international partners, advanced substantial financial support mechanisms for Ukraine, reinforcing Europe’s role as a central pillar of regional stability. From an economic perspective, the IMF emphasized that sustained support was critical not only for Ukraine’s economy but also for containing broader regional risk.

However, these commitments carried fiscal implications. Increased borrowing needs, higher defense expenditures, and long-term reconstruction planning intensified debates around debt sustainability and burden sharing within the EU. Some member states expressed caution over joint financial obligations, highlighting persistent differences in fiscal philosophy across the Union. For citizens, these decisions underscored a defining reality of 2025: economic policy was inseparable from values, security, and collective responsibility.

Image

Figure 1: EU €1.8 Billion Support to Ukraine (European Union financial support to Ukraine under the Ukraine Facility (fifth regular payment).

Source: European Commission (2025).What this means for ordinary Europeans: This figure shows that Europe’s support for Ukraine in 2025 is no longer an emergency response, but a planned and predictable commitment. For citizens, it explains why public budgets include continued spending beyond national borders. The message is simple: stability in Europe’s neighborhood is seen as essential to long-term economic security at home, even if it requires sustained financial responsibility.

Labour Markets and Social Realities

One of the quieter successes of Europe’s economy in 2025 was the continued resilience of labour markets. Data from Eurostat, supported by analysis from the European Commission, showed employment levels remaining high across much of the EU, with unemployment rates stabilizing near historic lows.

This resilience reflected structural labor shortages in certain sectors, as well as the lingering effects of earlier fiscal and employment support. As inflation moderated and confidence improved, job creation continued though unevenly across regions. Yet stable employment did not automatically translate into improved living standards.

According to the OECD and European Commission consumer surveys, cumulative price increases for essentials particularly food, housing, and energy continued to outpace nominal wage growth when assessed over multiple years. As a result, many households felt that purchasing power had not fully recovered, even as headline inflation eased. The disconnect between macroeconomic stabilization and lived experience became a defining social undercurrent of 2025. Policymakers increasingly acknowledged that price stability alone was insufficient if income growth and perceived fairness lagged behind.

In the United Kingdom, still navigating post-Brexit adjustments, the Office for National Statistics and the Bank of England reported continued pressure on real household incomes, driven by elevated essential costs and structural labor market frictions. While inflation stabilized, the cost-of-living challenge persisted as a central political and economic issue.

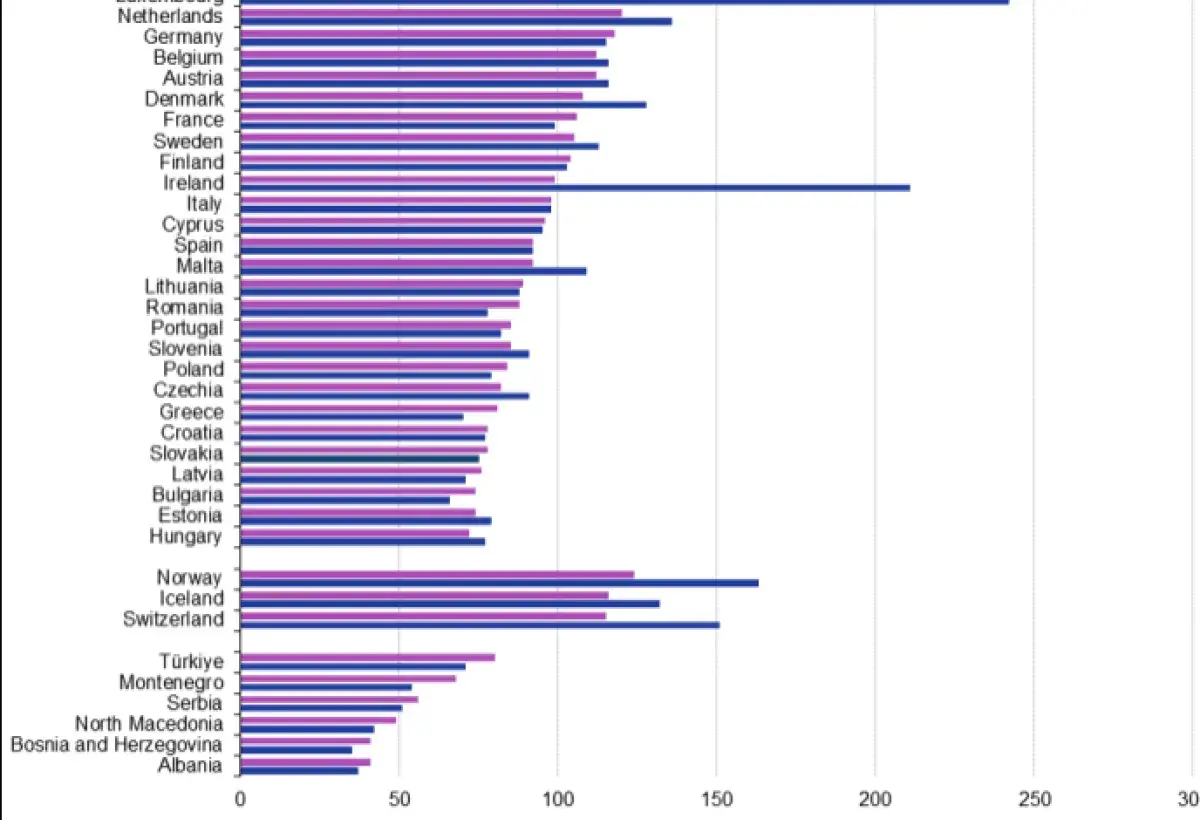

Image

Figure 2: GDP vs. Actual Individual Consumption (AIC) per Person (Source: Eurostat, online data code: prc_ppp_ind)

What this means for daily life: This graph helps explain why people in different European countries experience living standards differently even when national income levels appear high. While GDP shows how much an economy produces, AIC reflects what people actually consume, including public services like healthcare and education. The smaller gaps in AIC reveal how social systems help cushion inequalities, making everyday life more comparable across countries despite wide differences in economic output.Energy remained a structural concern in 2025, even as Europe moved beyond the emergency phase of the energy crisis.

According to the International Energy Agency, Europe entered 2025 with significantly more diversified energy supply routes than before 2022, including higher liquefied natural gas imports and expanded intra-EU interconnections. However, energy prices remained structurally higher than pre-crisis norms, particularly for energy-intensive industries. Europe’s long-term strategy anchored in diversification, efficiency, and accelerated renewable investment continued under EU-level frameworks and national transition plans. These efforts strengthened long-term energy security but imposed short-term adjustment costs.

European Commission surveys indicated broad public support for energy independence, tempered by concerns over affordability and the social distribution of transition costs. By year’s end, energy policy had firmly shifted from emergency response to strategic transformation.

Fiscal Pressures and Public Debt

Fiscal dynamics remained a central concern across the EU in 2025. Higher public spending on defense, healthcare, and social protection combined with modest revenue growth pushed debt ratios higher in several member states.

The European Commission projected slight increases in general government deficits absent corrective measures. While inflation nearing target helped stabilize interest costs, fiscal consolidation challenges loomed, particularly in countries with long-standing debt vulnerabilities. For citizens, these debates were tangible: public debt influenced taxes, services, and political priorities. The central policy tension of 2025 became how to balance investment, solidarity, and fiscal sustainability.

Public Perception: Stability Without Euphoria

By late 2025, economic sentiment surveys presented a nuanced picture:

What improved

-

Inflation approached target levels (ECB, IMF)

-

Employment remained resilient (Eurostat)

-

Europe demonstrated strategic cohesion in the face of geopolitical stress

What remained challenging

-

Growth stayed below historical averages (IMF)

-

Cost-of-living pressures lingered (OECD, European Commission)

-

Recovery remained uneven across regions

Conclusion: A Year That Changed the Conversation

Europe’s economy in 2025 was not defined by spectacle, but by durability amid constraint. Growth was steady, inflation normalized, and crisis management gave way to complex tradeoffs. Economists will remember 2025 as a transition year one that restored stability while exposing unresolved structural limits. Citizens will recall a year of cautious predictability, tempered by ongoing pressure on household budgets. The enduring lesson of 2025 is this:

Progress in modern Europe is measured not by speed, but by the capacity to endure, adapt, and choose deliberately under constraint.

Author’s Reflection

Europe’s 2025 experience underscores a critical policy truth: stability is meaningful only when citizens can feel it in daily life. While institutions succeeded in restoring macroeconomic balance, many households remained constrained by weak income growth and persistent cost pressures. This gap between policy success and public experience now defines the next challenge. The lesson of 2025 is not that Europe must act faster, but that it must act fairer aligning fiscal discipline, growth strategy, and social protection so economic resilience becomes tangible security for its people.

Image

References

European Union Institutions

European Central Bank. (2025). Economic Bulletin and monetary policy decisions, 2025.

https://www.ecb.europa.eu/press/economic-bulletin/html/index.en.html

European Central Bank. (2025). Monetary policy statements and staff macroeconomic projections.

https://www.ecb.europa.eu/press/pressconf/html/index.en.html

European Commission. (2025). Autumn 2025 Economic Forecast: Continued growth amid a challenging environment.

https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/economic-forecasts/autumn-2025-economic-forecast_en

European Commission. (2025). EU economic governance and fiscal outlook.

https://economy-finance.ec.europa.eu/economic-and-fiscal-governance_en

Eurostat. (2025). GDP, employment, and unemployment statistics.

https://ec.europa.eu/eurostat/statistics-explained/index.php?title=Main_Page

International Financial and Economic Institutions

International Monetary Fund. (2025). World Economic Outlook: Navigating global divergence.

https://www.imf.org/en/Publications/WEO

International Monetary Fund. (2025). Regional Economic Outlook: Europe.

https://www.imf.org/en/Publications/REO/Europe

Organisation for Economic Co-operation and Development. (2025). OECD Economic Outlook.

https://www.oecd.org/economic-outlook/

Organisation for Economic Co-operation and Development. (2025). Consumer price trends and household income.

https://www.oecd.org/economy/inflation.htm

Energy and Infrastructure Authorities

International Energy Agency. (2025). Europe energy outlook and gas market report.

https://www.iea.org/reports

International Energy Agency. (2025). Energy security and transition pathways in Europe.

https://www.iea.org/topics/energy-security

European Network of Transmission System Operators for Gas. (2025). European gas system and market assessments.

https://www.entsog.eu

Thanks for these photos Lazerkong, and Reshoots-com on Pixabay.